Bertrand issued $10 million convertible loan notes on 1 October 2010 that carry a nominal

Bertrand issued $10 million convertible loan notes on 1 October 2010 that carry a nominal interest (coupon) rate of 5% per annum. They are redeemable on 30 September 2013 at par for cash or can be exchanged for equity shares in Bertrand on the basis of 20 shares for each $100 of loan. A similar loan note, without the conversion option, would have required Bertrand to pay an interest rate of 8%.

When preparing the draft financial statements for the year ended 30 September 2011, the directors are proposing to show the loan note within equity in the statement of financial position, as they believe all the loan note holders will choose the equity option when the loan note is due for redemption. They further intend to charge a finance cost of $500,000 ($10 million x 5%) in the income statement for each year up to the date of redemption.

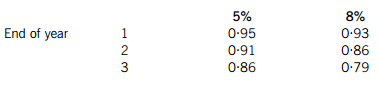

The present value of $1 receivable at the end of each year, based on discount rates of 5% and 8%, can be taken as:

Required:

(a) (i) Explain why the nominal interest rate on the convertible loan notes is 5%, but for non-convertible loan notes it would be 8%. (2 marks)

(ii) Briefly comment on the impact of the directors’ proposed treatment of the loan notes on the financial statements and the acceptability of this treatment. (3 marks)

(b) Prepare extracts to show how the loan notes and the finance charge should be treated by Bertrand in its financial statements for the year ended 30 September 2011. (5 marks)

请帮忙给出正确答案和分析,谢谢!

-

暂无相关推荐

-

(a) On 1 January 2015 Palistar acquired 75% of.....

-

Crag Co has sales of $200m per year and the gross profit margin is 40%. Finished goods inv..

-

CSC Co is a health food company producing and selling three types of high-energy products:..

-

Robber Co manufactures control panels for burglar alarms a very profitable product. Every..

-

Which of the following statements is/are correct? 1 An increase in the cost of equity lead..

-

Section B – TWO questions ONLY to be attemptedAs.....

冀公网安备 13070302000102号

冀公网安备 13070302000102号